Markets and Economy Is the angst over AI spending and Fed inaction warranted?

August 3, 2026

Our framework continues to point to a global economy that’s in a slowdown regime, as growth still remained above its long-term trend but gradually decelerated.1

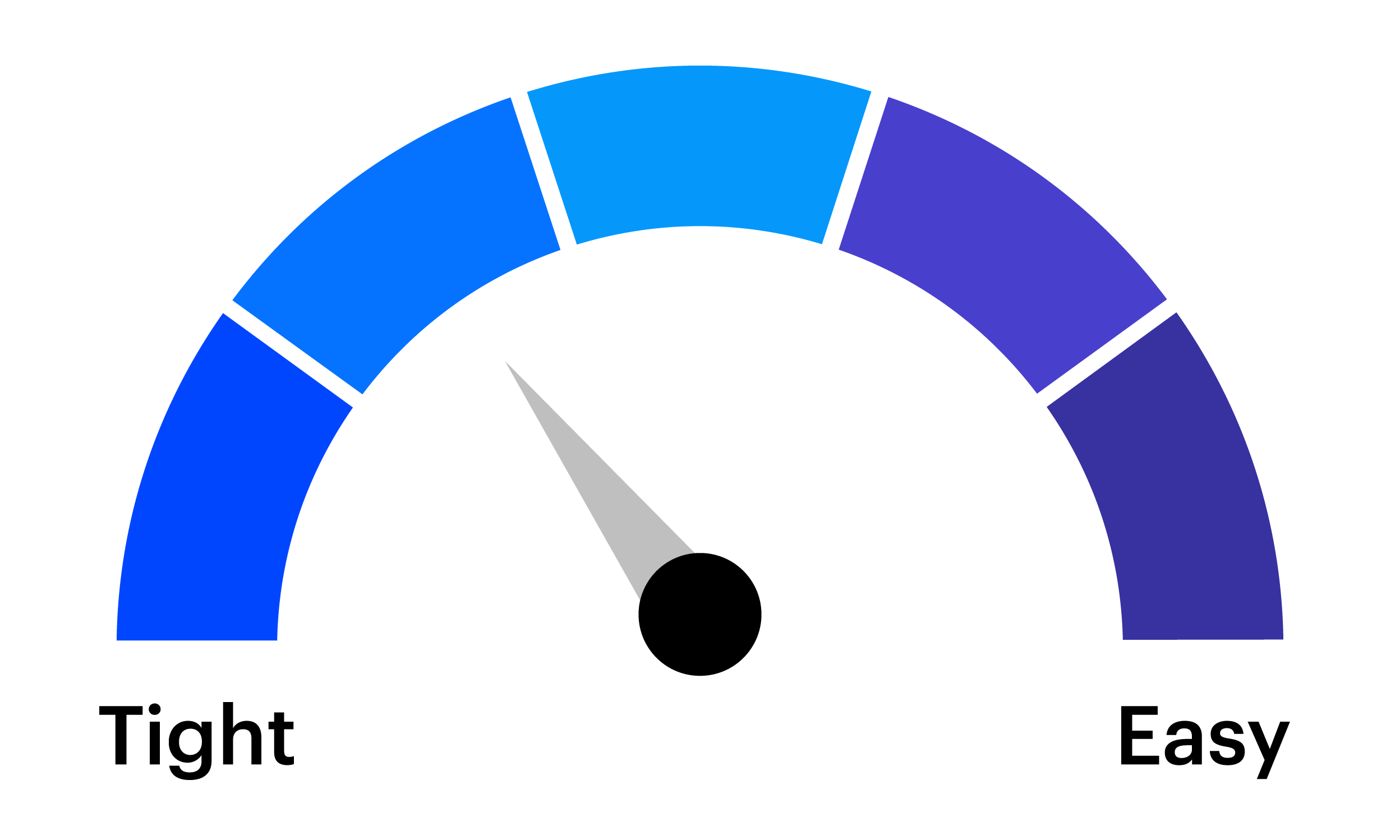

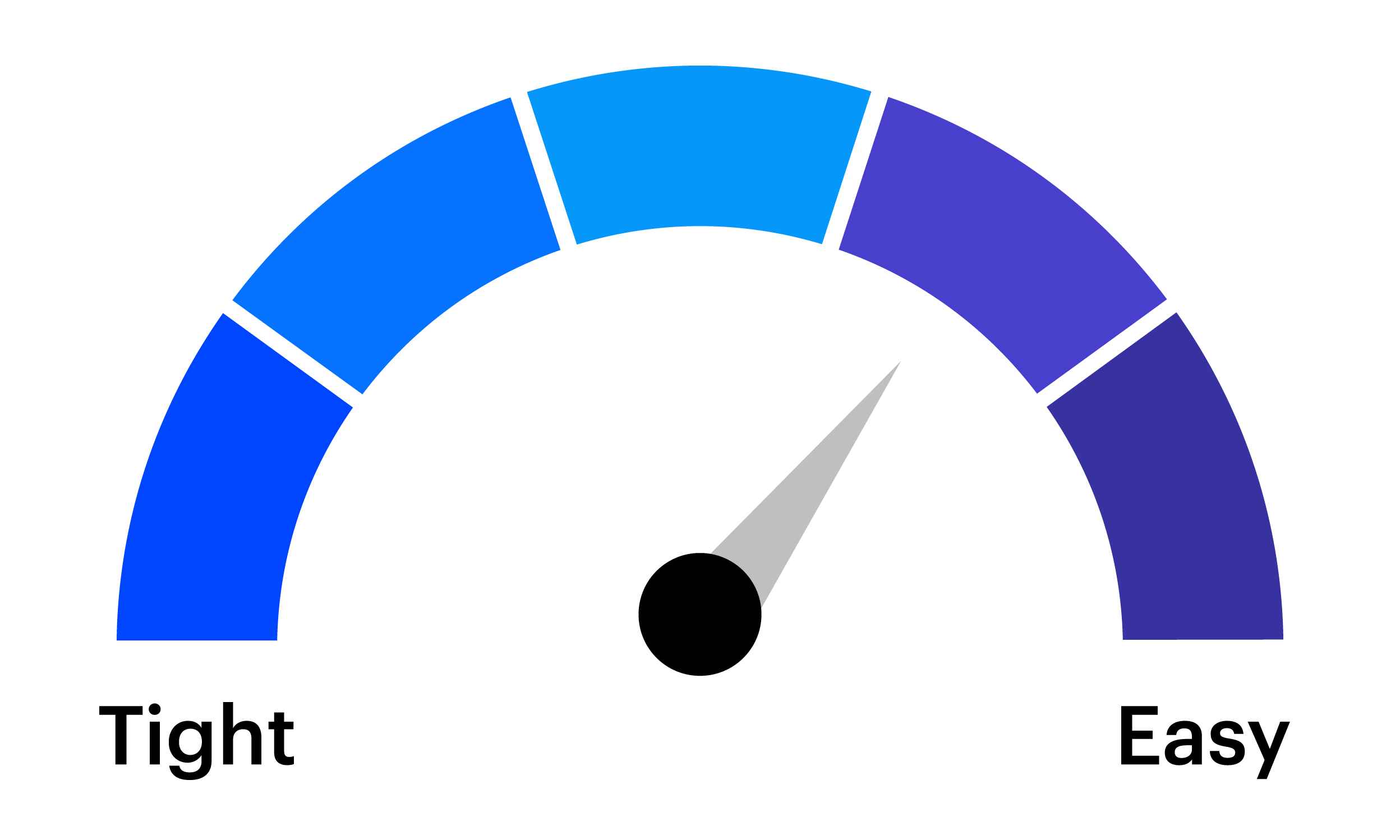

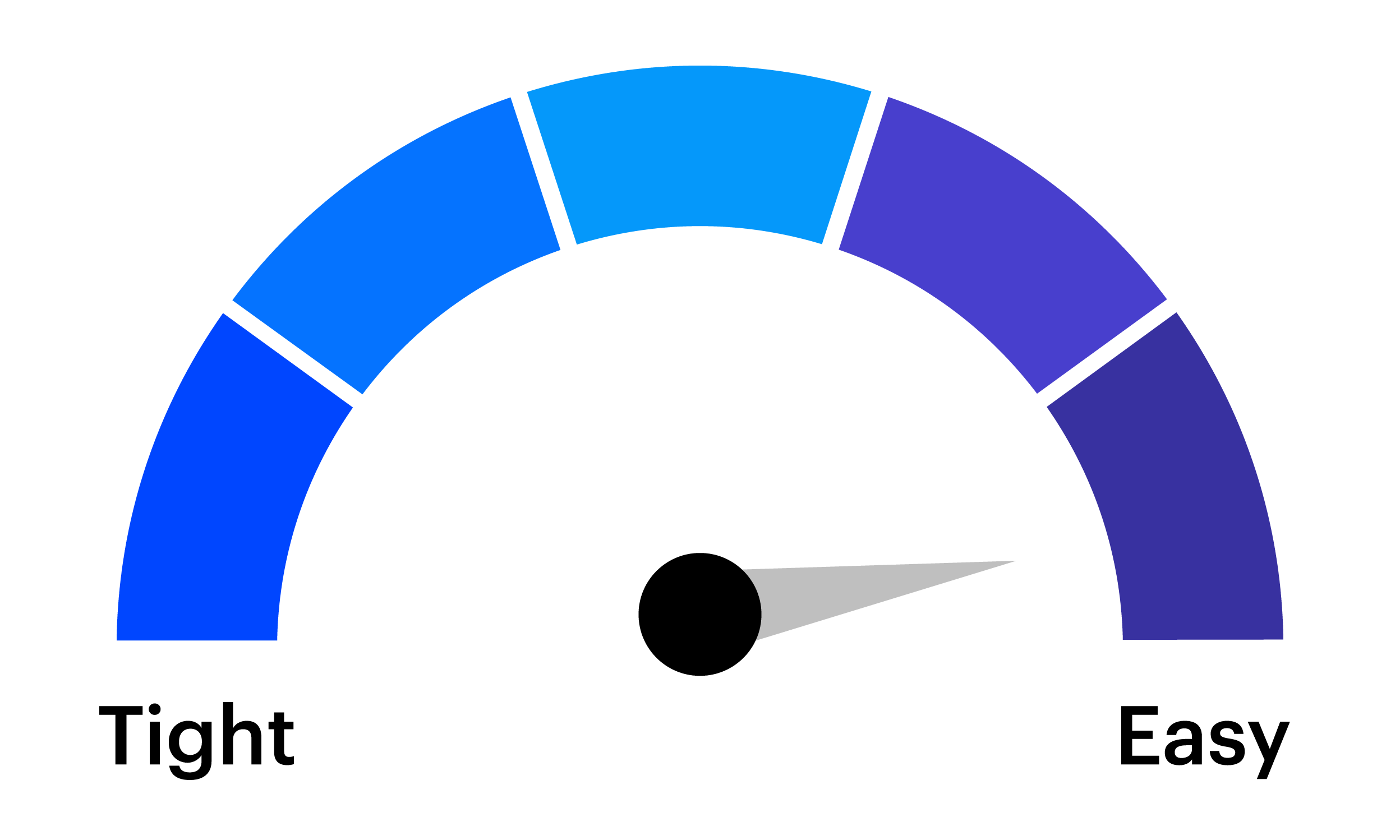

Easing energy prices, lower inflation momentum, and falling market-implied inflation expectations have shifted the macro backdrop. But increasingly hawkish central bank policy has pushed real interest rates higher and tightened financial conditions, leading to a transition from inflation-led uncertainty toward policy-driven constraint. These dynamics may support a regime of above-trend but slowing growth rather than a cycle-ending contraction.

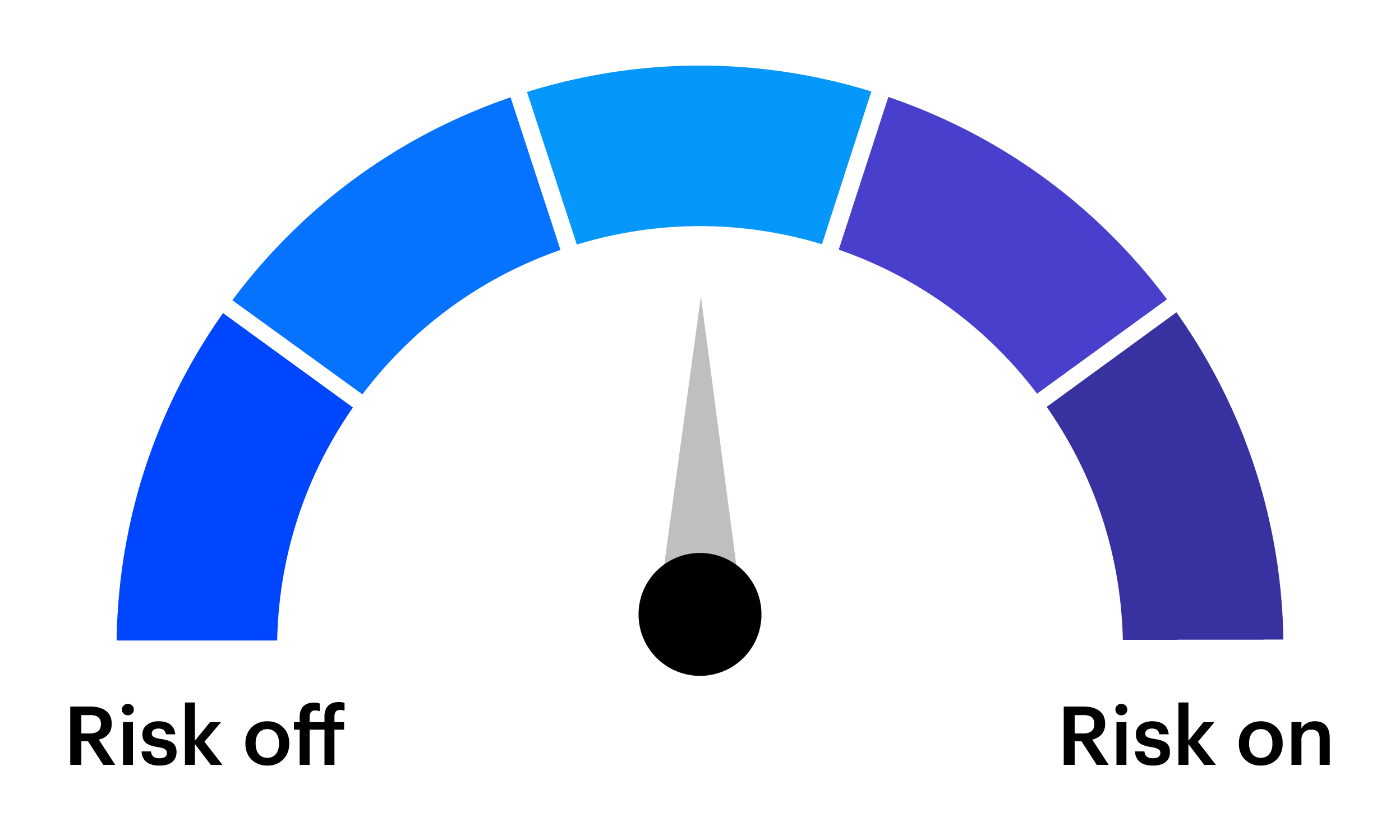

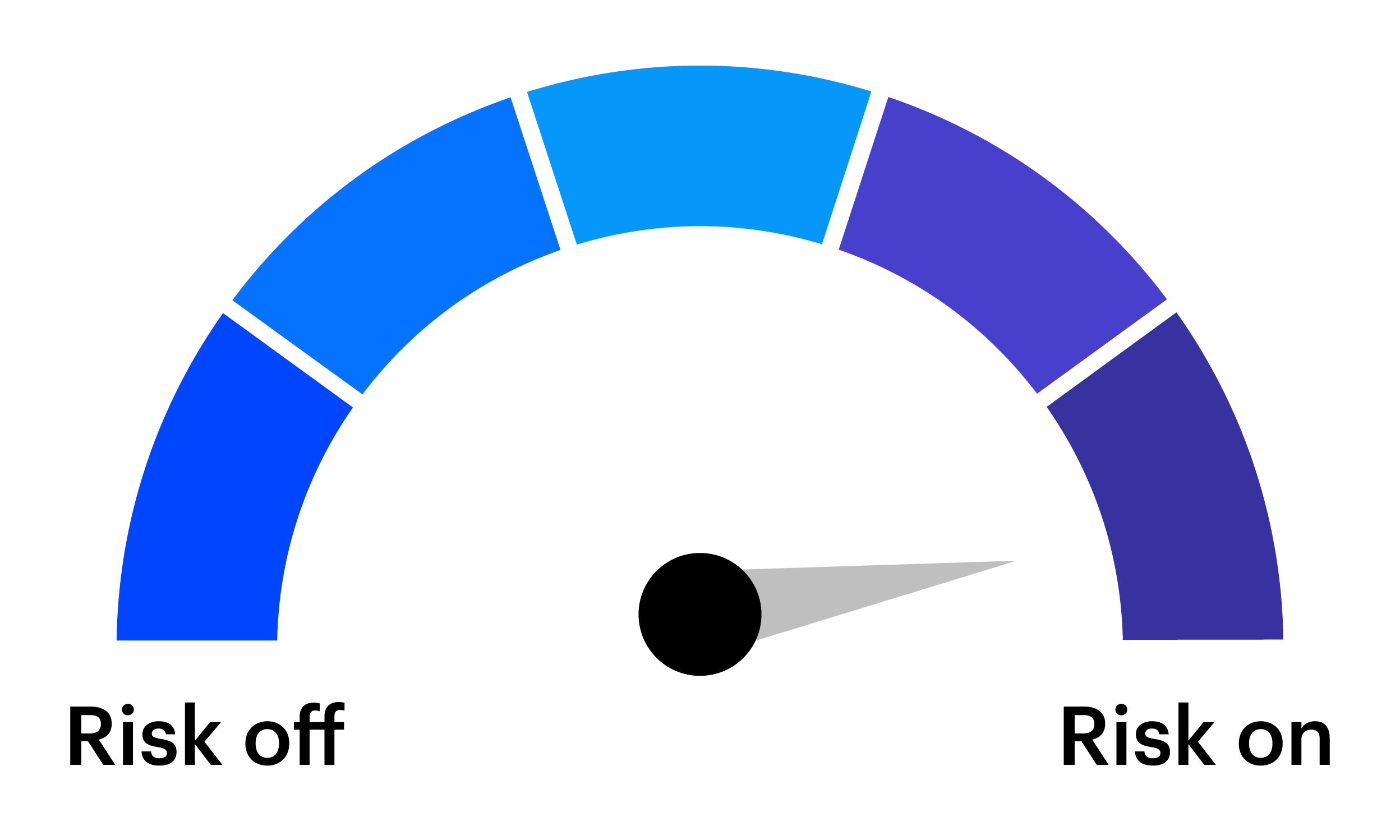

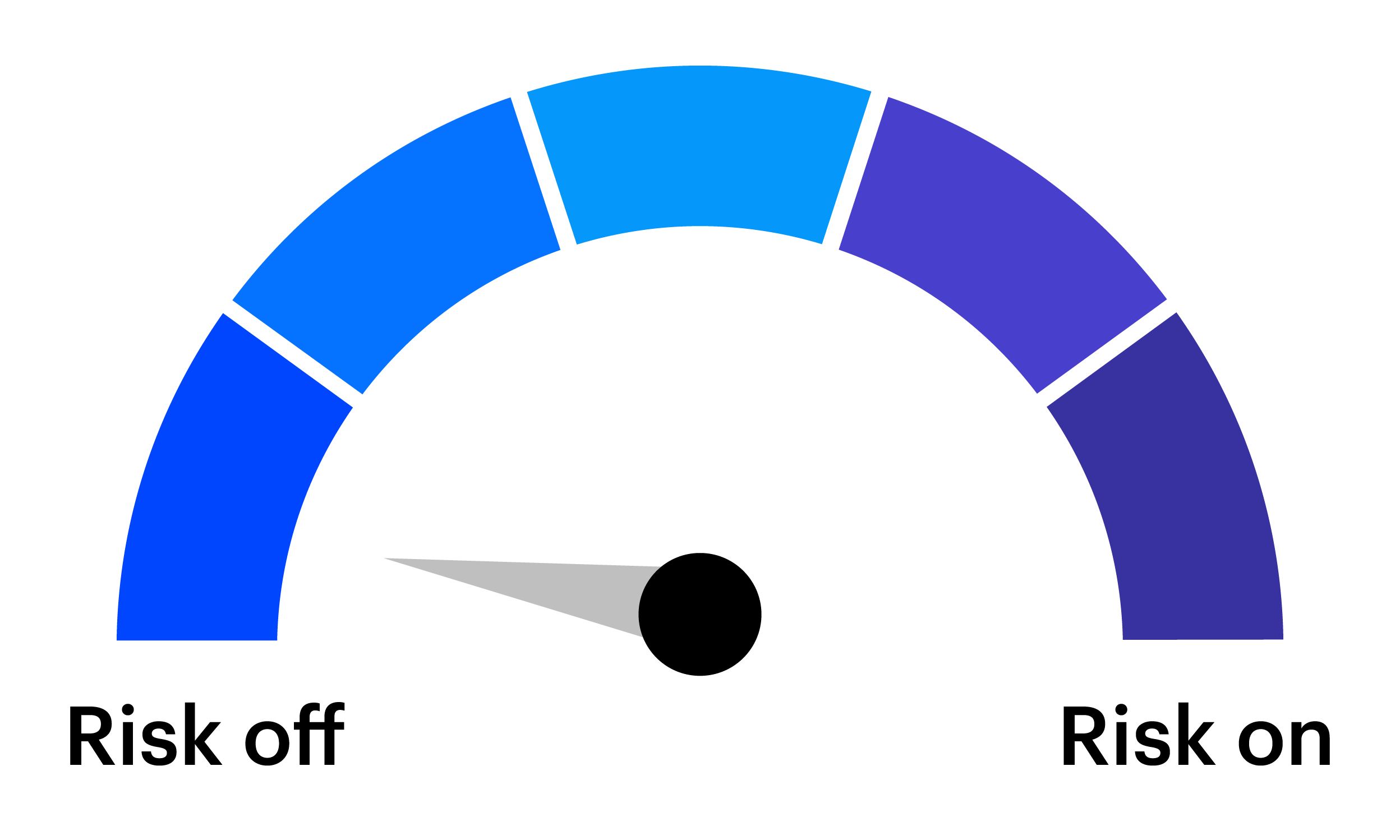

As a result, we emphasize diversification and risk management. We remain moderately overweight stocks over bonds, continue to favor defensive factors and sectors, and incrementally reduced our preference for US relative to developed non-US markets. We’re maintaining an overweight to duration, an underweight to credit risk, and have reduced our preference for the US dollar as improving international growth may support developed non-US markets.

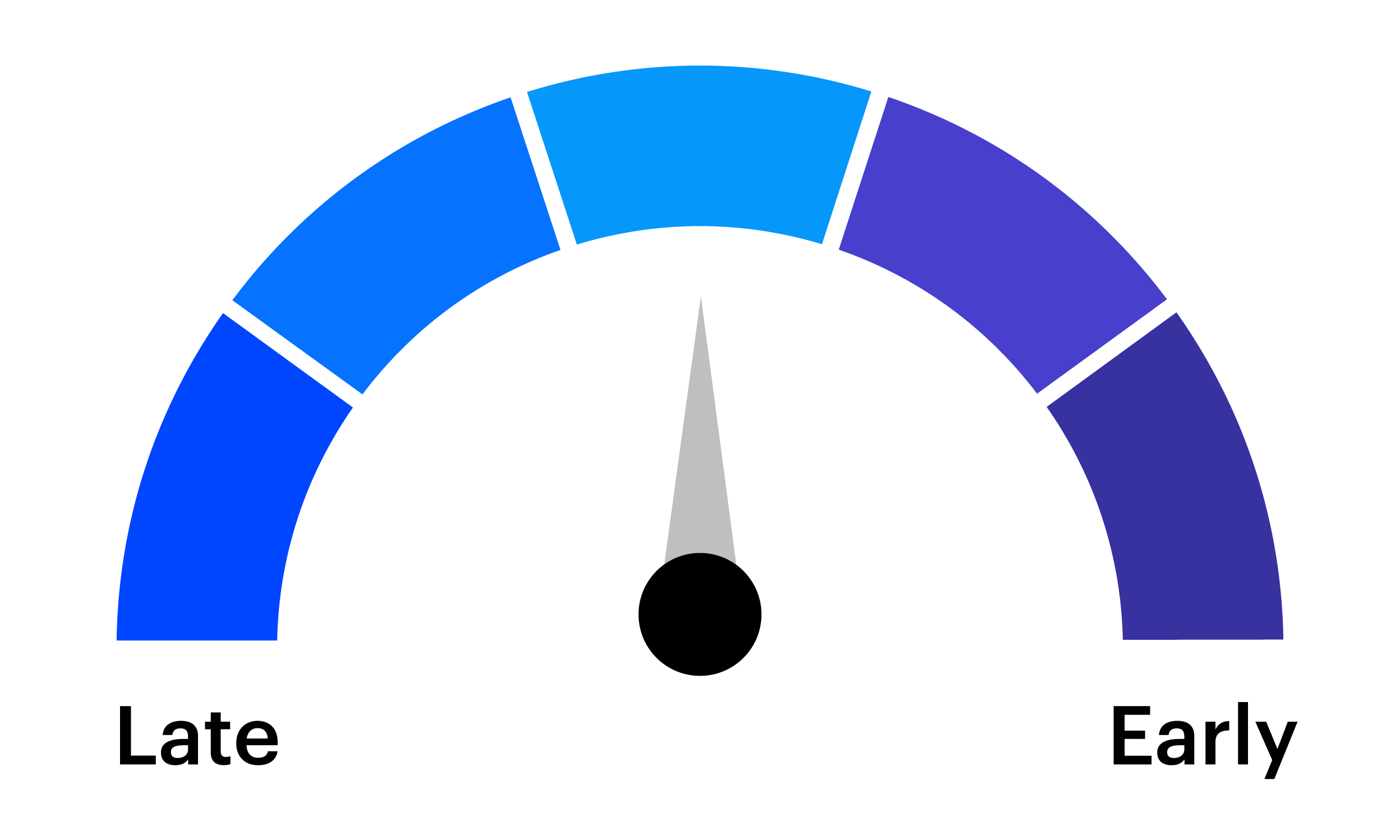

A challenge for tactical investors is preparing for the expected and anticipating the unexpected. The tactical asset allocation (TAA) framework from the Invesco Solutions team is designed to enhance a long-term strategic asset allocation (SAA) by making portfolio tilts based on near-term market views.

The tactical, dynamic factor rotation shown below is also utilized in the Invesco Russell 1000® Dynamic Multifactor ETF (OMFL).

Explore further research and analysis from our market and investment experts.

NA5721358

Duration is a measure of the sensitivity of the price (the value of principal) of a fixed income investment to a change in interest rates. Duration is expressed as a number of years.

Diversification does not guarantee a profit or eliminate the risk of loss.

Larger, more established companies may be unable to respond quickly to new competitive challenges such as changes in consumer tastes or innovative smaller competitors. Returns on investments in large capitalization companies could trail the returns on investments in smaller companies.

Class Y shares are closed to most investors. Please see the prospectus for more details.

Tightening is a monetary policy used by central banks to increase interest rates to slow economic growth and curb inflation.

This does not constitute a recommendation of any investment strategy or product for a particular investor. Investors should consult a financial professional before making any investment decisions.

Past performance does not guarantee future results. An investment cannot be made directly into an index.

All investing involves risk, including the risk of loss.

Some products are offered through affiliates of Invesco Distributors, Inc.

The opinions referenced above are those of the author as of July 2026. These comments should not be construed as recommendations, but as an illustration of broader themes. Forward-looking statements are not guarantees of future results. They involve risks, uncertainties, and assumptions; there can be no assurance that actual results will not differ materially from expectations.

Tightening is a monetary policy used by central banks to normalize balance sheets.

There are risks involved with investing in ETFs, including possible loss of money. Index-based ETFs are not actively managed. Actively managed ETFs do not necessarily seek to replicate the performance of a specified index. Both index-based and actively managed ETFs are subject to risks similar to stocks, including those related to short selling and margin maintenance. Ordinary brokerage commissions apply. The Fund's return may not match the return of the Index. The Fund is subject to certain other risks. Please see the current prospectus for more information regarding the risk associated with an investment in the Fund.

Growth stocks tend to be more sensitive to changes in their earnings and can be more volatile.

A value style of investing is subject to the risk that the valuations never improve or that the returns will trail other styles of investing or the overall stock markets.

Stocks of small- and mid-sized companies tend to be more vulnerable to adverse developments, may be more volatile, and may be illiquid or restricted as to resale.

Fixed income investments are subject to credit risk of the issuer and the effects of changing interest rates. Interest rate risk refers to the risk that bond prices generally fall as interest rates rise and vice versa. An issuer may be unable to meet interest and/or principal payments, thereby causing its instruments to decrease in value and lowering the issuer’s credit rating.

Credit spread is the difference between Treasury securities and non-Treasury securities that are identical in all respects except for quality rating.

Alternative products typically hold more non-traditional investments and employ more complex trading strategies, including hedging and leveraging through derivatives, short selling and opportunistic strategies that change with market conditions. Investors considering alternatives should be aware of their unique characteristics and additional risks from the strategies they use. Like all investments, performance will fluctuate. You can lose money.

The risks of investing in securities of foreign issuers, including emerging market issuers, can include fluctuations in foreign currencies, political and economic instability, and foreign taxation issues.

Junk bonds involve a greater risk of default or price changes due to changes in the issuer’s credit quality. The values of junk bonds fluctuate more than those of high quality bonds and can decline significantly over short time periods.

In general, stock values fluctuate, sometimes widely, in response to activities specific to the company as well as general market, economic, and political conditions.

Municipal securities are subject to the risk that legislative or economic conditions could affect an issuer’s ability to make payments of principal and/ or interest.

An investment in emerging market countries carries greater risks compared to more developed economies.