Insight Understanding Investment Trusts

Investment trusts have been used by private investors for over 150 years to grow their wealth, deliver an income, or a combination of the two. With a choice of strategies, they offer a range of options to help realise your financial ambitions. In this Investment Trust Education Hub, we explore how they work, how investors can use them in a portfolio and what makes them different from other types of collective investment.

Investment trusts: harnessing a world of opportunity

Investment trusts are collective investments that pool your capital with those of other investors to target capital growth or income. Our explainers look at the features that differentiate them from other funds, including gearing (borrowing to make additional investments), the way income is treated, and the flexibility they give fund managers. They also explore the diversity within the sector, and the role they can play for those investors looking for income, and those looking to build their wealth.

What is an investment trust and what can they bring to a portfolio?

Investment trusts let you invest in a range of different asset classes, regions and sectors. They are run as public limited companies and are listed on the London Stock Exchange. They have an independent board that appoints the investment manager, monitors their performance, and looks after the interests of shareholders.

Download our summary guides:

What is an Investment Trust?

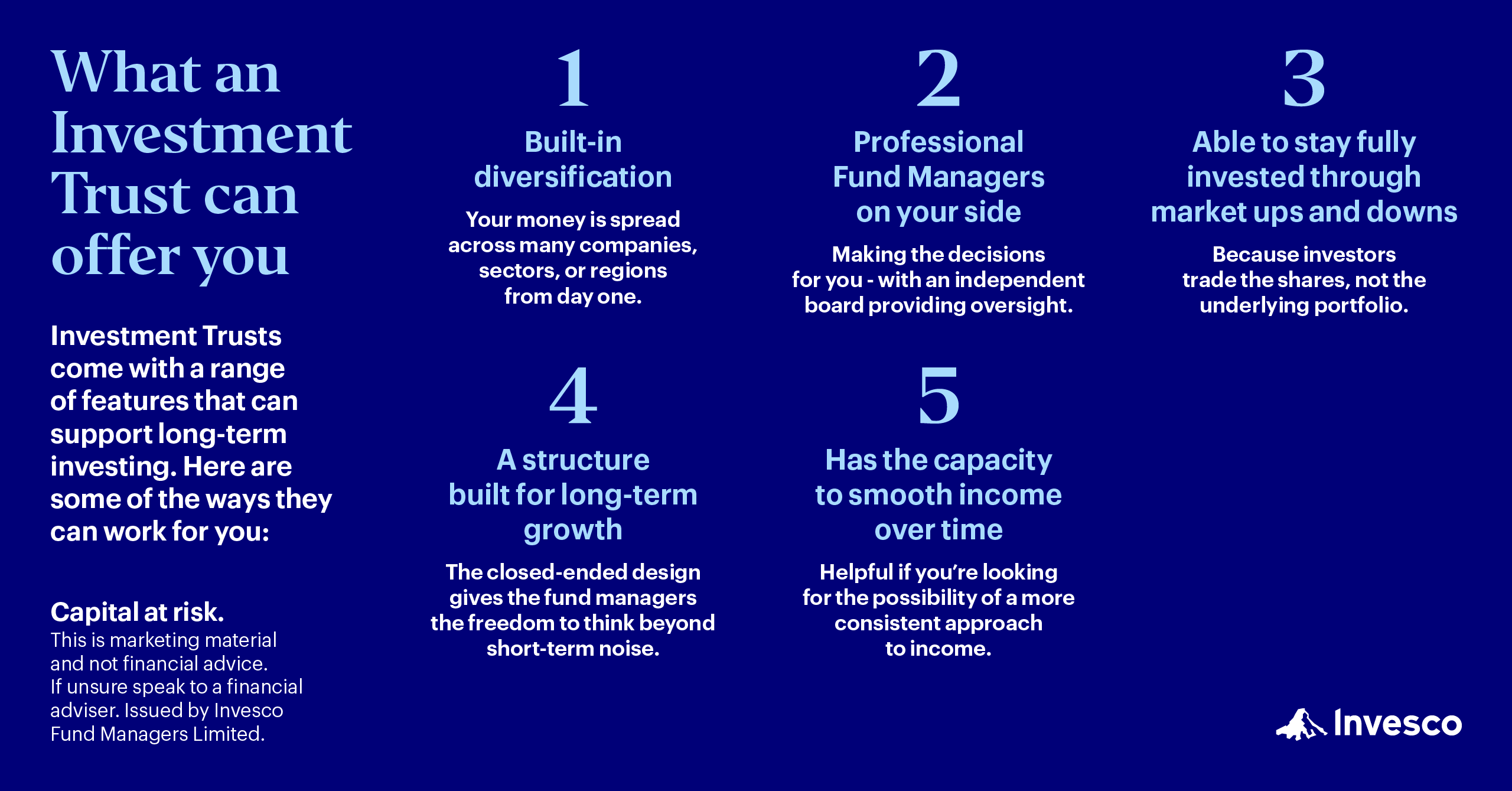

What an Investment Trust can offer you

{kind=link}

{kind=link}

Investing with investment trusts

With almost 300 UK-listed investment trusts to choose from, there are options for investors wanting to grow their wealth, or to generate an income. We explore their unique characteristics and how you can find the right investment trust for your financial goals.

How to use investment trusts

The investment trust sector is diverse, and trusts can play a range of roles in a portfolio. They can be an option for growing wealth ahead of retirement, while many trusts aim to deliver an income in your later years. They can be used for education planning, or to build a nest egg for children.

Investment trusts for retirement income

In retirement, your income needs to be reliable and consistent, but it also needs to grow over time, defending you against inflation. Many investment trusts have a well-established track record of growing their payouts to shareholders every year for decades. The structure of investment trusts helps them do this, allowing them to reserve income in good times to pay out in more difficult conditions. Investment trusts may have a role to play in supporting your income needs in retirement.

Building a diversified portfolio with investment trusts

One of the best defenses investors have against the highs and lows of markets is diversification. Diversification is about spreading your investments across a variety of sectors, regions and asset classes. Investment trusts can help you build a diversified portfolio.

Comparing investment trust performance

Analysing investment trust performance is about more than just picking last year’s star performer. It is important to get the right fit for you, with a trust that matches your risk parameters, capital growth ambitions and your income needs. We look at how you can compare investment trusts to find the best long-term option for you.

Investment trusts vs funds

Unlike an open-ended fund (such as a unit trust or an open-ended investment company), investment trusts are structured as public companies. This creates certain key differences. For example, they are listed on a stock exchange, so their share price is driven by supply and demand and can be different to the value of the underlying holdings. They can borrow to invest, reserve income to pay out at a later date, and may have more investment flexibility. Find out more about the key differences between investment trusts and funds.

FAQs

The investment trust universe is large and diverse, giving investors a wealth of options to meet their financial goals. Investment trusts have certain unique characteristics that can support investors’ ambitions for capital growth or a consistent income. They are as easy to buy and sell as normal shares, through brokers, investment platforms or your financial adviser.

Every investment trust is unique and has its own risk and reward characteristics. Investors need to look under the bonnet at the type of assets in which a trust invests to understand its risks. Trusts should be treated as longer-term investments and your capital is at risk.

Investment trusts may target capital growth, income, or a combination of the two. These targets will be clearly set out in the trust’s objectives. The investment trust’s board should hold the investment manager to account and ensure they meet those objectives. You should look for an investment trust where the objectives match your own.

Investment trusts can invest in a range of assets, including shares and bonds, but also commercial property, infrastructure, or private equity. The ‘closed-ended’ structure of investment trusts gives them greater flexibility to invest in illiquid asset classes. These are assets such as bricks and mortar property or infrastructure assets that cannot readily be bought and sold.

While investment trusts and open-ended investment companies (OEICs) have some elements in common, there are some important distinctions between the two structures. Investment trusts are listed on a stock exchange, which means the price is determined by supply and demand for the shares. Investment trusts have a board, which is tasked with holding the investment management company to account. Also, investment trusts are ‘closed-ended’, which means they have a fixed pool of assets.

Fund managers will invest the assets of a trust in line with its objectives. They will use their skill, judgement and experience to invest, and may also have a strong team of analysts supporting them. The fund managers are held to account by the board, who can change the investment manager if they don’t believe the objectives have been met.

Investment trusts are well-regulated. They are structured as public limited companies, and are therefore subject to UK company law and the Financial Conduct Authority Listing Rules. Trusts also agree to comply with the Association of Investment Companies Code of Corporate Governance, and London Stock Exchange rules. Investment trusts must appoint a board of governors to look after shareholder interests and are also required to make disclosures to the stock exchange and to shareholders. However, they are products where your capital is at risk. They will invest in financial markets, where pricing can be volatile and your investment can go down as well as up.

EMEA5498974